Why Most Dental Service Organizations Underperform After Roll Up

- A dental service organization owns the non-clinical operating stack for a group of dental practices, so each dentist can focus on patients instead of payroll.

- The DSO model is a private equity multiple arbitrage play, and marketing efficiency is one of the levers that moves the exit multiple.

- Most twenty-clinic groups quietly lose six figures a year on duplicate ad accounts, orphaned Google Business Profiles, and fragmented analytics.

- A consolidated marketing stack across all clinics delivers roughly thirty percent lower cost-per-call than running each clinic's program in parallel.

- Smile Design Dentistry moved PPC conversion up twenty percent and cost per call down thirty percent by consolidating across fifty-plus locations.

A dental service organization pools the back-office work of a group of practices under one operating team so each clinic can focus on chairside care. On paper that sounds like clean gain. In real life, the average DSO wastes six figures a year on redundant Google Business Profiles, split analytics, and per-location websites that no one keeps current. This is a plain-English look at what a dental service organization actually does, where the model quietly loses money, and how growing groups tighten the marketing side so a fifteen-clinic roll-up performs like one brand instead of fifteen tabs open at once.

What a dental service organization is

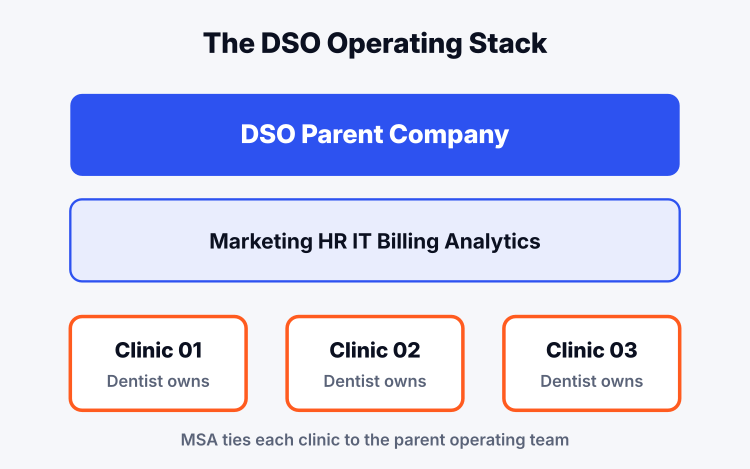

A dental service organization, or DSO, is a parent company that supplies non-clinical services to a network of affiliated dental practices. The dentist owns the clinic. The DSO owns the machinery around it. That machinery covers marketing, HR, payroll, accounting, IT, procurement, credentialing, insurance contracting, and a shared analytics stack that rolls fifteen clinics into one dashboard. The clinical care stays with the licensed provider. Every state has slightly different corporate practice of dentistry rules, and the DSO structure is designed to sit within those rules. Read how a dental DSO is structured for the corporate anatomy under the hood.

The reason the model exists is scale. A single-clinic dentist spends fifteen hours a week doing things that have nothing to do with teeth. A DSO absorbs those fifteen hours across ten, fifty, or five hundred clinics and hires specialists for each function. A regional DSO with forty offices has a dedicated marketing lead, a dedicated recruiter, a dedicated revenue cycle manager, and a real IT team. A single clinic has the office manager doing all four jobs badly. That is the trade the DSO model sells, and when it is run well it works.

The DSO marketing side is the piece most groups get wrong. The clinics were bought from independent owners who each built their own website, their own Google listing, their own review pipeline, and their own vendor stack. Nothing was standardized. The roll-up team inherits fifteen versions of a marketing program and either rebuilds it under one system or lets each clinic keep running on its own, which is where the money quietly leaves.

How a dental service organization is structured

The corporate shell of a DSO sits above the clinics. Under it are the affiliated practices, each still owned on paper by a licensed dentist in states that require it. The DSO buys the practice’s non-clinical assets and signs a long-term management services agreement with the clinic entity. The dentist keeps clinical control and often keeps equity in the parent. The DSO handles everything else and takes a management fee tied to collections.

Ownership of a modern DSO usually traces back to private equity. A sponsor buys a platform of ten to twenty clinics, then rolls up smaller practices around it over three to seven years. The math is simple. A single dental office sells at four to six times EBITDA. A network of forty offices under one operating team sells at eight to twelve times. Every clinic added compresses the multiple gap between what the sponsor paid and what the platform is worth on exit. Marketing efficiency is one of the levers that moves those numbers.

The org chart inside a well-run group looks like this. A CEO, a CFO, a chief clinical officer, a chief marketing officer, a director of operations, regional directors covering five to ten clinics each, and a shared services team in a single office handling billing, credentialing, HR, and marketing. The clinics report metrics upward on a weekly cadence. Provider retention, patient acquisition cost, new patient volume, case acceptance rate, and collections per operatory are the numbers that move the meetings.

The three flavors of DSO you actually see in the market

Not every dental service organization runs the same playbook. The market has settled into three broad shapes, and the marketing approach that works inside each one is different. Groups that copy a national DSO’s playbook without matching its scale usually spend more and grow slower than they need to.

| DSO type | Clinic count | Brand model | Marketing approach |

|---|---|---|---|

| National platform | 500+ | Single brand across all offices | Centralized creative, national media buying, one website with per-location pages |

| Regional roll-up | 15 to 200 | Master brand or holding brand with sub-brands | Shared analytics stack, per-clinic Google Business Profiles, unified website with location pages |

| Affiliated group | 3 to 20 | Individual clinic brands preserved | Shared vendors, each clinic keeps its own website, coordinated review generation |

Heartland Dental, Aspen Dental, and Pacific Dental Services run the national platform model. They rebrand every acquired clinic and route all traffic through one website. Regional roll-ups like Smile Brands and MB2 Dental sit in the middle, keeping some sub-brands and centralizing the rest. Affiliated groups let each clinic keep its identity and only share the back-office work. Each model has trade-offs, and the marketing playbook has to match the shape the sponsor picked when the group was formed.

The mistake we see most often is a fifteen-clinic regional roll-up trying to run national platform tactics. They centralize the website too fast, kill the individual clinic identities that patients trusted, and watch new patient volume drop for six months before the new brand catches on. A slower rebrand paired with strong per-clinic local SEO ranking factors work protects the revenue as the master brand is built.

Where the marketing side loses money inside a DSO

Every roll-up we have audited has the same four sources of underperforming spend, and they are boring. No one loses a hundred thousand dollars a year on strategy. They lose it on tools nobody canceled, duplicate ad accounts nobody consolidated, and per-clinic vendors nobody replaced. The dollars quietly compound as the operations team focuses on clinical integration, which is where the real risk feels bigger.

Leak one is the duplicate stack. Each acquired clinic came in with its own Google Ads account, its own Meta Business Manager, its own CallRail or CallTrackingMetrics contract, its own Hubspot or Kareo instance, and often two separate SEO vendors. A twenty-clinic group we audited in 2024 was paying $47,000 a year across duplicate call-tracking, review platforms, and reporting tools that a single stack could have covered for under $12,000. That is one full salary lost to overlap.

Leak two is orphaned Google Business Profiles. When a DSO buys a practice, the seller’s personal Gmail account still owns the GBP. Six months later the seller has stopped answering emails, the DSO cannot post updates or respond to reviews from the corporate account, and Google’s ownership transfer process takes three to eight weeks per listing. A thirty-clinic group with fifteen unclaimed profiles is invisible in the map pack until someone runs the transfer for every single one. That is a straight revenue hit until it is fixed.

Leak three is analytics fragmentation. Each clinic has its own Google Analytics 4 property, its own Search Console, its own ad account. Rolling that up into one dashboard so the CFO can see cost per new patient by clinic and by service line takes either a data engineer or a shared services team that already knows how. Most DSOs skip this for the first two years, run on gut feel, and only fix it after a bad quarter forces the question. Leak four is per-clinic websites that share nothing. Fifteen different themes, fifteen different hosting bills, fifteen different content update cycles, and no shared design system. See our note on healthcare web design that earns patient trust for the pattern that actually works across a network.

How Smile Design Dentistry consolidated fifty locations

The clearest picture of what a DSO marketing rebuild looks like is Smile Design Dentistry, a Dade City, Florida DSO that grew from a single office in 2004 to more than fifty locations across Central Florida and the Tampa Bay area. When they came to us in 2022, tracking was limited, targeting was broad, paid social was not running, and the marketing dollars were spread across per-clinic vendors with no shared reporting layer.

We restructured the PPC accounts under one corporate Google Ads and Meta setup, added full-funnel paid social including dental TikTok ads with retargeting keyed to each location’s service radius, and built per-location landing pages inside a single unified template so a patient searching cosmetic dentistry near their zip code landed on the right clinic without a rebuild for every service line. Tracking flowed through CallRail into a shared reporting dashboard that the operations team pulled weekly.

The numbers over the engagement moved in three directions at once. PPC conversion rate went up 20 percent year over year as the paid stack got smarter about which searches converted into booked patients. Cost per call dropped 30 percent as duplicate spend disappeared and the ad accounts consolidated learning across all fifty offices instead of relearning bid strategy separately at each clinic. Every one of the fifty-plus locations went live on the new stack with per-location reporting that the CFO and each regional director could pull without waiting on an agency. That is the pattern that plays for a DSO of this size, and the pieces of it stack the same way whether the group has fifteen offices or five hundred.

What growing DSOs get wrong most often

The pattern of mistakes across DSOs at the twenty to fifty clinic mark is remarkably consistent. Groups this size are past the point where per-clinic marketing works and not yet at the scale where a national brand pays for itself. That in-between zone is where most of the operating pain shows up, and where the biggest returns on tight marketing operations sit.

The first common mistake is over-centralizing too early. Killing the individual clinic brand names before the master brand has any local search authority erases three to five years of trust the seller built. New patient volume drops for six to nine months as the new brand catches up. A slower, staged rebrand keyed to a master brand plus clinic tagline, then a full rebrand once the map pack rankings hold, protects the revenue during the transition.

The second is under-investing in the front desk. Every dollar the marketing side spends to generate a lead is wasted if the call answer rate is 60 percent and the average call-to-booking conversion is 22 percent. A DSO that hires a centralized patient coordination team, records calls, and coaches to a script gets to 90 percent answer rates and 55 percent call-to-book conversion. That single lever moves cost per new patient more than any ad optimization does. The third is treating each clinic’s Google Business Profile as an afterthought. See our Local Services Ads for dentists guide for the piece the map pack now sits on top of. And the fourth is skipping dental review generation as a corporate program instead of a per-clinic hope.

What a fifteen-clinic marketing stack looks like

The tools list for a mid-size DSO is shorter than most people think. One Google Ads MCC account with sub-accounts per region. One Meta Business Manager with pixel access across every clinic domain. One call tracking platform with dynamic number insertion at the clinic level. One SEO reporting stack. One CRM or PMS integration point that ties phone calls, form fills, and online bookings to the source that produced them. That is the whole stack, and it replaces what most twenty-clinic groups run across nine or ten separate vendors.

| Function | Fragmented setup | Consolidated DSO stack |

|---|---|---|

| Paid search | 15 separate Google Ads accounts | 1 MCC with location sub-accounts |

| Call tracking | Mix of CallRail and CallTrackingMetrics per clinic | 1 platform with dynamic numbers |

| Websites | 15 different themes on 15 hosts | 1 platform with per-location pages |

| Analytics | 15 GA4 properties, no roll-up | Shared dashboard across all clinics |

| Reviews | Manual per-clinic asks | Automated post-visit review request across the network |

The savings on tools is only part of the return. The bigger gain is that the ad accounts and analytics start learning across all fifty offices at once. Google’s bid algorithms need conversion data to work. A single-clinic account with fifteen bookings a month never gives the algorithm enough signal to optimize. A consolidated network account with 750 bookings a month across fifty clinics does. The same paid dollars produce better results since the machine has more to learn from. That is the real reason multi-location marketing under one team beats fifteen versions of the same program run in parallel.

Frequently asked questions about dental service organizations

What does a dental service organization do that a private practice does not

A dental service organization handles every part of running a practice that is not chairside clinical care. That covers marketing, HR, payroll, IT, credentialing, insurance contracting, billing, and analytics across every affiliated clinic under one operating team. The dentist keeps clinical control and often keeps equity in the parent company.

A private practice dentist ends up doing all of those jobs personally or hiring an office manager who does them halfway. The DSO trade-off is giving up some autonomy in exchange for professional back-office support at scale. A well-run DSO frees the dentist to see 25 percent more patients per week since they are no longer spending Thursday afternoons on payroll and vendor calls. A poorly run one becomes another layer of overhead that just takes a management fee.

How large is a typical dental service organization

Dental service organizations range from three-clinic affiliated groups to national platforms with over 1,000 offices. The median regional DSO in 2024 operates 15 to 60 clinics in a single state or two neighboring states. National platforms like Heartland Dental, Aspen Dental, and Pacific Dental Services each run 500 to 1,700 offices.

Size matters for the marketing approach. A three-clinic group runs a shared vendor list. A twenty-clinic group needs a consolidated ad account and shared analytics. A hundred-clinic group needs a full in-house marketing team with agency support layered on for specialist work. The playbook that works at fifteen clinics breaks at fifty, and the one that works at fifty breaks at five hundred. Sizing the marketing stack to the current clinic count and the growth plan for the next 24 months is what separates the DSOs that scale cleanly from the ones that keep replatforming every 18 months.

Why do private equity firms invest in dental service organizations

Private equity invests in dental service organizations for multiple arbitrage. A single dental office sells at four to six times EBITDA. A network of 40 or more offices under one operating team sells at eight to twelve times. Every clinic rolled up compresses that gap between purchase multiple and exit multiple.

The other draw is recession resilience. Dental care demand is steady across economic cycles. Insurance reimbursements are more predictable than most healthcare verticals. Cash-pay procedures like cosmetic and implant work grow with median household income. A dental service organization gives a private equity sponsor a defensible platform that generates 15 to 25 percent EBITDA margins with consistent same-store growth. That combination is rare in healthcare, which is why capital keeps flowing into the sector.

How does a dso dental service organization market itself differently

A dso dental service organization markets both to patients and to selling dentists. Patient-facing marketing runs on the master brand or the individual clinic brands, focused on local search, paid ads, and reviews. Seller-facing marketing runs on the parent brand, focused on operators considering an acquisition or affiliation deal.

The dual audience shapes the website structure. Most DSO sites have a patient path leading to per-clinic booking pages and a separate careers-and-affiliation path leading to a deal team. The best-run groups treat the seller path as seriously as the patient path, since a single closed acquisition adds 12 to 24 months of new patient revenue that no ad campaign can generate on its own. See our healthcare SEO strategy guide for how the two audience layers stack inside one architecture.

Is a dental service organization the same thing as a corporate dental practice

A dental service organization is close to what most patients would call a corporate dental practice, but the legal structure is different. The DSO does not employ the dentist directly in most states. The dentist owns the clinic, and the DSO owns the management services agreement. That structure exists to comply with state corporate practice of dentistry laws that prohibit non-dentists from owning dental clinics.

From a patient perspective the experience feels similar to a corporate practice. Standardized care processes, uniform pricing, shared referral pathways to specialists inside the network, and a booking system that can move a patient between clinics if the primary provider is unavailable. From an operator perspective the DSO structure is a compliance choice more than a philosophical one. The parent company runs the business. The dentist runs the medicine. The line between the two is drawn by state law and enforced by the corporate structure.

See how we help multi-location dental groups tighten the marketing side of the operating model at our DSO marketing rollout page.

Book your free 30-minute strategy call.

No spam, no sales rep. We use your email to schedule your call with a senior strategist. That is it.

More from the blog

View all articles → Marketing Strategy

Marketing Strategy How Dental DSOs Grow Through Marketing. Tactics That Scale

Read article Marketing Strategy

Marketing Strategy Dental DSO Marketing Services. What to Expect From an Agency Partner

Read article Marketing Strategy

Marketing Strategy